![]()

Closing Entries Definition, Examples, and Recording

Dividend account is credited to record the closing entry for dividends. In addition, if the accounting system uses subledgers, it must close out each subledger for the month prior to closing the general ledger for the entire company. In addition, if the company uses several sets of books for its subsidiaries, the results of each subsidiary must first be transferred to the books of the parent company and all intercompany transactions eliminated. If the subsidiaries also use their own subledgers, then their subledgers must be closed out before the results of the subsidiaries can be transferred to the books of the parent company. Since the income summary account is only a transitional account, it is also acceptable to close directly to the retained earnings account and bypass the income summary account entirely. In the above case, a net credit of ₹ 55,00,000 or profit will finally be moved to the retained earnings account by debiting the Income summary account.

- From the Deskera “Financial Year Closing” tab, you can easily choose the duration of your accounting closing period and the type of permanent account you’ll be closing your books to.

- Now for this step, we need to get the balance of the Income Summary account.

- Expense accounts have a debit balance, so you’ll have to credit their respective balances and debit income summary in order to close them.

- Closing entries are mainly used to determine the financial position of a company at the end of a specific accounting period.

- Hence, strong accounting regulations and policies restrict the public listed companies from abusing certain loopholes while producing their financial reports.

Unit 4: Completion of the Accounting Cycle

Permanent Account entries show the long-standing financial position of a company. Thebalance in the Income Summary account equals the net income or lossfor the period. This balance is then transferred to the RetainedEarnings account.

Financial Accounting

They are special entries posted at the end of an accounting period. Below are the T accounts with the journal entries already posted. We’ll use a company called MacroAuto that creates and installs specialized exhaust systems for race cars.

Step 2: Close Expense accounts

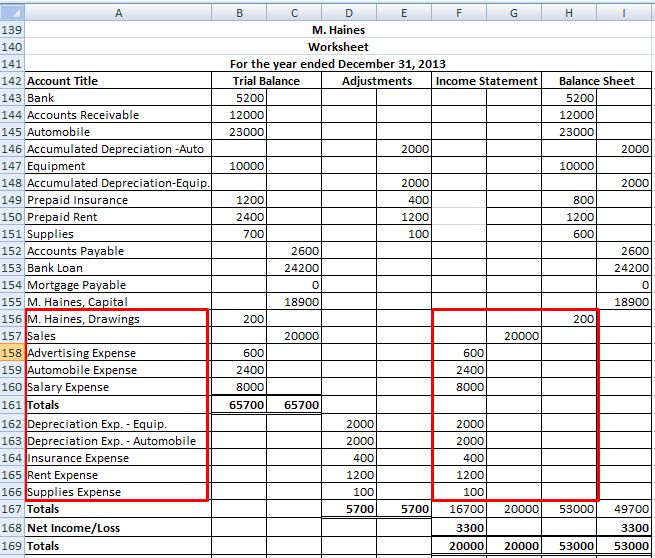

Let’s explore each entry in more detail using Printing Plus’sinformation from Analyzing and Recording Transactions and The Adjustment Process as our example. The Printing Plusadjusted trial balance for January 31, 2019, is presented inFigure 5.4. It is the end of the year,December 31, 2018, and you are reviewing your source documents for accounting transactions financials for theentire year. You see that you earned $120,000 this year in revenueand had expenses for rent, electricity, cable, internet, gas, andfood that totaled $70,000. LiveCube Task Automation is designed to automate repetitive tasks, improve efficiency, and facilitate real-time collaboration across teams.

He is the sole author of all the materials on AccountingCoach.com. For the past 52 years, Harold Averkamp (CPA, MBA) has worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. Double Entry Bookkeeping is here to provide you with free online information to help you learn and understand bookkeeping and introductory accounting. We follow strict ethical journalism practices, which includes presenting unbiased information and citing reliable, attributed resources. The articles and research support materials available on this site are educational and are not intended to be investment or tax advice.

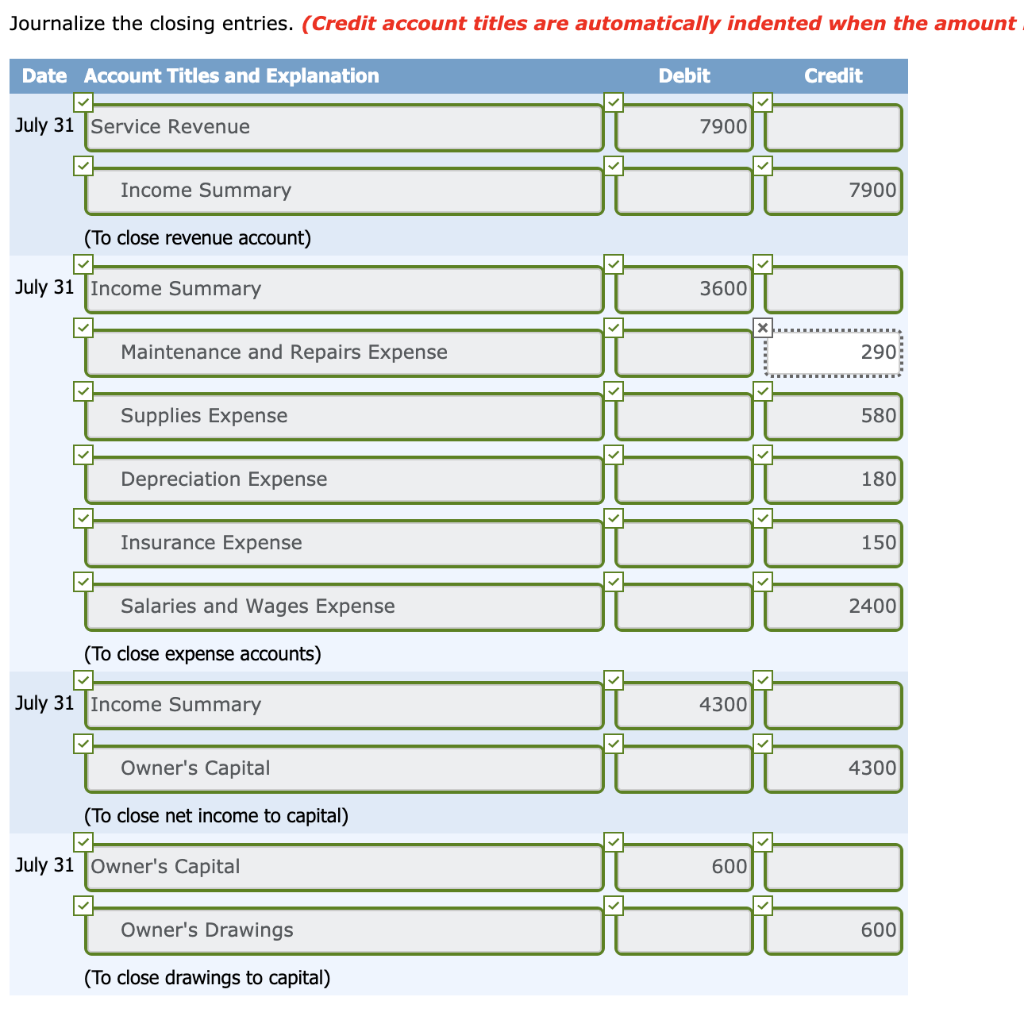

To close revenue accounts, you first transfer their balances to the income summary account. Start by debiting each revenue account for its total balance, effectively reducing the balance to zero. Then, credit the income summary account with the total revenue amount from all revenue accounts. Closing entries are a fundamental part of accounting, essential for resetting temporary accounts and ensuring accurate financial records for the next period. This process highlights a company’s financial performance and position.

The four closing entries are, generally speaking, revenue accounts to income summary, expense accounts to income summary, income summary to retained earnings, and dividend accounts to retained earnings. We see from the adjusted trial balance that our revenue accounts have a credit balance. To make them zero we want to decrease the balance or do the opposite. We will debit the revenue accounts and credit the Income Summary account. The credit to income summary should equal the total revenue from the income statement. The permanent accounts in which balances are transferred depend upon the nature of business of the entity.

Closing all temporary accounts to the retained earnings account is faster than using the income summary account method because it saves a step. There is no need to close temporary accounts to another temporary account (income summary account) in order to then close that again. After preparing the closing entries above, Service Revenue will now be zero. The expense accounts and withdrawal account will now also be zero. At the end of a financial period, businesses will go through the process of detailing their revenue and expenses.